The market sold off “AI trades” while second-tier fabs raised prices and boosted capex. Defense ministries tightened vendor lists while AI labs clarified what “classified” actually means. A robotaxi blew a basic social norm. A viral app went dark because one cloud vendor hiccuped.

The connective tissue isn’t hype or capability. It’s dependency.

Who you depend on for compute. Who your customers depend on for trust. Who your investors depend on for macro beta. And increasingly, who your regulators depend on for plausible deniability.

If your AI roadmap assumes stable inputs, cheap GPUs, tolerant regulators, patient capital, and invisible infra, yesterday was a reminder: the real risk isn’t that models get smarter. It’s that your dependency graph is already too fragile for the systems you’re trying to build on top.

BLUF

At Neue Alchemy, we support leaders navigating inflection points, when tech, capital, and policy converge. If your roadmap is already in motion and you’re pressure-testing execution, we’re open to conversations.

We also reserve capacity for education, SMBs, and mid-market leaders, those starting, mid-flight, or seeking outside perspective before systems harden.

INFRASTRUCTURE / COMPUTE

AI hardware is a seller’s market, and second-tier fabs just confirmed it

Asia’s smaller chipmakers are joining larger peers in hiking prices as AI demand drives projected semiconductor capex up 25% YoY to more than $136B in 2026, per Nikkei Asia.

These are not the flagship foundries setting the tone, this is the second tier realizing they can raise prices and still justify aggressive expansion.

The Bet: AI demand will stay strong enough that even non-leading-edge fabs can both raise ASPs and grow capacity without triggering a demand shock.

So What? AI infra is no longer just constrained at the bleeding edge. When trailing and specialty nodes are repricing and expanding, the entire hardware stack, accelerators, controllers, networking, storage, is repricing with it. If you’re assuming “GPU prices will normalize” in your 2027–2028 models, you’re fighting both capex momentum and vendor pricing power. The structural shift: compute is behaving like energy, a strategic input whose price is set by global demand and capex cycles, not your individual contract.

The Risk: If macro or regulatory shocks slow AI workloads, late-cycle capex could overshoot, flipping bargaining power back to buyers, but with a 2–3 year lag. In the meantime, over-optimistic infra startups that underprice capacity on the assumption of falling costs will get squeezed hardest.

Action: • Lock in multi-year capacity and pricing where you can, especially for non-bleeding-edge nodes that underpin networking, storage, and embedded AI. • Rewrite your unit economics with a “high compute cost” scenario and see which products still clear hurdle rates. Kill or delay the rest. • If you’re a startup selling infra, anchor pricing to value delivered, not your current COGS, your input costs are on a rising curve.

PLATFORMS / DEFENSE ALIGNMENT

AI labs, NATO, and the new vendor whitelist reality

An OpenAI spokesperson clarified that Sam Altman “misspoke” when saying the company was looking to deploy on NATO classified networks, the target is unclassified NATO networks, per Reuters.

In parallel, the US Department of Defense’s ban on Anthropic usage is now extending into primes like Lockheed Martin, which will follow the federal order, per Reuters.

The Bet: AI labs and defense ecosystems are both assuming that “where” a model runs, classified vs unclassified, approved vs banned vendor, is now as material as “what” the model can do.

So What? Defense and national security are becoming the highest-stakes reference customers for foundation models. That pulls AI labs into a procurement regime where vendor lists, export controls, and classification boundaries are hard constraints. If you’re building on a given lab’s stack, your own eligibility in defense, aerospace, and critical infrastructure will be downstream of their regulatory posture, not just your own. This is a structural fork: some stacks will be “defense-aligned,” others “consumer/enterprise-first.” Straddling both without a clear story will get harder.

The Risk: A fast-moving ban or policy shift can strand your product if it’s tightly coupled to a disfavored vendor, especially in regulated or public-sector markets. Miscommunication, like “classified” vs “unclassified”, can trigger political scrutiny that outpaces your actual technical risk profile.

Action: • Map your model dependencies against current and likely government vendor lists, including bans, in your key markets. Treat this as a go/no-go gate for public-sector and defense GTM. • For any defense-adjacent roadmap, maintain at least one “policy-safe” model option, even if it’s less capable, and validate it technically this quarter. • Tighten comms discipline: if you sell into government or critical infrastructure, align marketing, sales, and legal on exactly what environments you support and what data you touch.

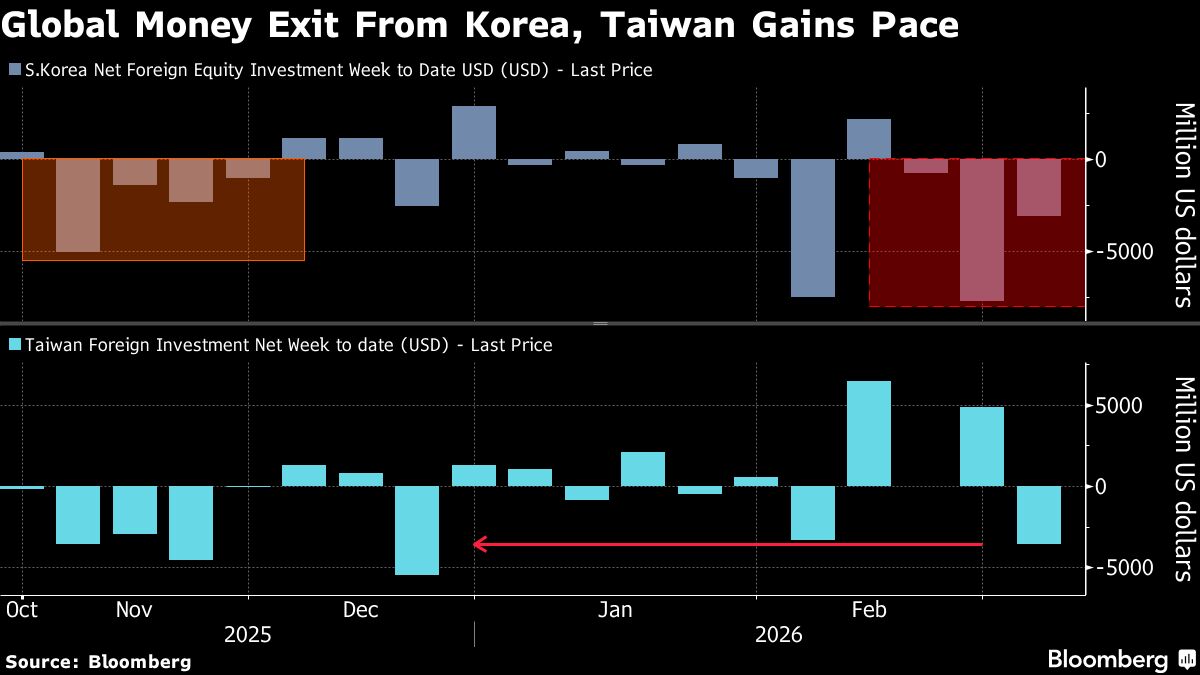

CAPITAL FLOWS / MACRO

AI beta is now macro beta, and your runway is exposed

Global funds are unwinding some of the “hottest AI trades” as oil supply fears and inflation concerns rise, per Bloomberg.

This isn’t about any single company missing numbers, it’s portfolio managers rotating out of crowded AI names when macro risk spikes elsewhere.

The Bet: AI is now a crowded, high-beta trade that gets trimmed first when risk sentiment turns, regardless of underlying execution.

So What? If your valuation, fundraising prospects, or employee comp are tied to public AI multiples, your fate is now partially set by oil headlines and inflation prints. This decouples operating performance from financing conditions in the short term, you can be executing well and still see your cost of capital jump or your equity comp lose motivational power. The structural shift: AI is no longer a niche growth story. It’s part of the core risk-on/risk-off machinery of global capital.

The Risk: Teams that internalized 2023–2025 valuation levels as “normal” will over-hire and over-commit on opex, assuming they can always roll into the next round at a premium. If macro tightens further, late-stage rounds will reprice first, compressing exit options for earlier-stage companies that were banking on strategic takeouts.

Action: • Re-forecast runway under a flat or down-round scenario for your next raise, and decide now what you’d cut to extend 12–18 months without new capital. • If you’re public or late-stage, revisit equity-heavy comp plans; consider shifting a slice to cash or RSUs with more conservative growth assumptions. • In vendor negotiations, assume your customers are also feeling this volatility, build pricing and contract structures that de-risk long-term commitments for them.

CLOUD / RELIABILITY

TikTok’s Oracle outages are a warning shot on single-cloud dependency

TikTok experienced another major outage tied to Oracle infrastructure, its second Oracle-linked incident in a month, disrupting service for users and creators, per Gizmodo.

TikTok’s US operations are deeply entangled with Oracle due to political and regulatory pressures, turning what would normally be a multi-cloud architecture into a constrained, single-vendor dependency.

The Bet: You can run a cultural-scale app, and a geopolitical flashpoint, on a single primary cloud and still maintain acceptable reliability and political cover.

So What? If a platform at TikTok’s scale can be knocked offline twice in a month by issues tied to one cloud provider, the old “we’ll add multi-cloud later” posture is no longer defensible for anything that functions as a public square or critical customer touchpoint. For AI-native products, the risk is higher: outages don’t just break UX, they break trust in automation and decision-making, which is harder to rebuild than DAUs. The structural point: cloud choice is no longer just a cost and performance decision. It’s a resilience and sovereignty decision, and in some cases, a political one.

The Risk: Regulators and lawmakers can use reliability incidents as additional leverage to push for architectural changes, data localization, mandated partners, or even forced divestitures. If your infra is tightly coupled to a single vendor’s proprietary services, your migration and diversification options shrink exactly when you need them most.

Action: • Inventory your single points of failure at the cloud-provider level, services you cannot easily replace or replicate, and rank them by blast radius. • For any app that is a primary customer or citizen surface, put multi-region and at least a skeletal multi-cloud failover plan on this quarter’s roadmap, not “someday.” • In new deals, negotiate for portability, data egress terms, standard interfaces, and contractual support for multi-cloud patterns, before you’re locked in.

AUTONOMY / ROBOTICS

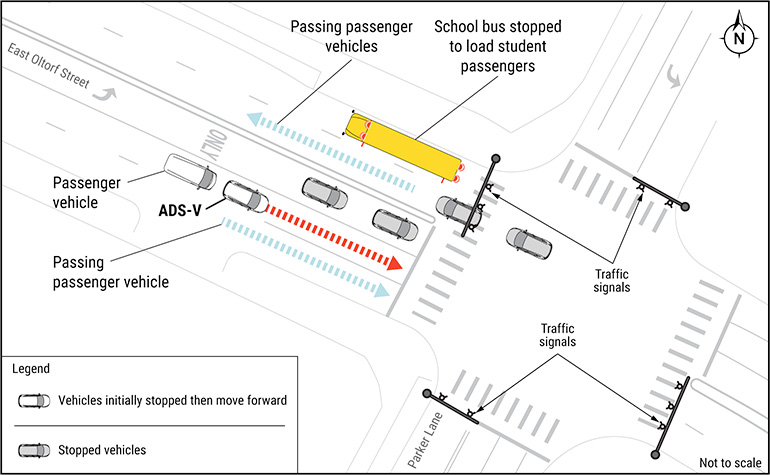

A Waymo robotaxi in Austin failed to stop for a school bus with its stop sign extended and lights flashing, an illegal maneuver that has triggered a federal investigation, per The Robot Report.

The vehicle reportedly passed the bus at low speed while children were disembarking, crossing a bright-line social and legal norm that humans are trained to treat as non-negotiable.

The Bet: Accumulated safe miles and technical performance will be enough to sustain public and regulatory support, even when rare but emotionally charged failures occur.

So What? This isn’t about perception accuracy in the abstract, it’s about violating one of the clearest “do not cross” rules in US driving culture. For operators, it underlines that autonomy deployments are now governed as much by social license and political optics as by disengagement rates. One high-salience failure can reset the Overton window on where and how you’re allowed to operate. The structural implication: autonomy rollouts will be gated by narrative management and incident response playbooks, not just safety cases and simulation data.

The Risk: A few more incidents in similarly sensitive contexts, school zones, emergency vehicles, pedestrians, could trigger broad moratoria or hyper-local bans that strand deployed capital. If your autonomy stack is deeply integrated into logistics or mobility operations, sudden regulatory pullbacks can blow up SLAs and customer trust overnight.

Action: • If you deploy autonomy, audit your “red line” scenarios, school buses, crosswalks, emergency scenes, and ensure they have explicit, conservative policies and test coverage. • Build a joint incident response protocol across engineering, legal, PR, and city partners, assume video of your next edge case will be online before your team is fully briefed. • If you’re a buyer of autonomy services, bake regulatory and social risk into contracts: termination rights, alternative routing, and manual fallback plans.

DATA / SURVEILLANCE

Adtech location data is now openly part of state surveillance

US federal agencies have used commercially available online advertising data to track the public’s phone locations, per Gizmodo.

Instead of going through telcos or obtaining warrants for specific devices, agencies tapped into adtech data streams, originally built for targeting and attribution, to reconstruct movement patterns.

The Bet: Commercial data exhaust is abundant and deniable enough that it can serve as a parallel surveillance channel without triggering the same legal and political constraints as traditional methods.

So What? If your product touches location or behavioral data, directly or via SDKs, you are now part of a supply chain that courts and regulators will treat as potential surveillance infrastructure. This changes the risk calculus: it’s not just about consent banners and privacy policies. It’s about whether your data flows can be compelled, discovered, or retroactively scrutinized in sensitive contexts. The structural shift: the line between “adtech” and “inteltech” has effectively collapsed.

The Risk: A high-profile case involving your data, even if you’re three hops removed, can trigger user backlash, regulatory action, and contractual scrutiny from enterprise customers. Future regulation could retroactively criminalize or heavily restrict certain data practices, leaving you exposed if you haven’t minimized collection and retention.

Action: • Map every path your app’s location and behavioral data takes, including third-party SDKs and partners, and document who can access what, and under what terms. • Minimize: stop collecting or retaining any location data you don’t actively use to deliver core value. “Nice to have” telemetry is now legal and reputational debt. • For enterprise and public-sector customers, be ready with a clear, auditable story on data provenance, retention, and law-enforcement access.

CONTRARIAN SIGNAL

“Mission” isn’t culture, it’s a compensation instrument

Dario Amodei highlighted that Anthropic’s retention is higher than OpenAI’s, emphasizing “mission” as a key lever to keep top researchers from defecting, per The Information.

The consensus read is soft: mission-driven cultures attract and retain better people. The harder read: in a market where cash and equity offers are converging, “mission” is being weaponized as a third leg of comp, a non-cash asset that still carries real economic value for the company.

If your story is fuzzy, your best people will treat you as a stepping stone, not because your salary bands are off by 10%, but because you haven’t given them a reason to discount higher external offers. Mission clarity is now part of total rewards design, not just an HR slide.

The Takeaway: If you’re competing for frontier talent and your “mission” can’t be stated in one sharp, non-generic sentence, you’re already paying a hidden tax in churn and recruiting friction.

THE QUESTION FOR TODAY

Compute vendors are raising prices and still ramping capex. Defense buyers are drawing hard lines on which AI stacks they’ll touch. Macro traders are treating your sector as a lever on oil and inflation risk. Your cloud, your data exhaust, and your autonomy stack are all new attack surfaces, for regulators, for users, for markets.

Does your current roadmap treat these dependencies as fixed background conditions, or as design variables you need to actively re-architect around this quarter?

See exactly how this impacts your specific industry and function. Upgrade to PRO to get bespoke tactical breakdowns generated instantly for your operating model.

Go deeper with the Weekly Signal

This is the daily take. The Weekly goes further — full strategic analysis across 8–10 sections, each with a signal read and operator action items. Source panel included.

Sign up free → then upgrade